For thousands of hardworking individuals across Malaysia, the dream of owning a home hits a frustrating dead end long before they ever step into a bank. It happens the moment a mortgage officer asks for three consecutive months of corporate payslips, an official tax statement, or a traditional employment contract. For small business owners, night market vendors, and gig economy workers within the Malaysian Indian community, these documents do not exist.

Their income is real, but to traditional financial institutions, they remain completely invisible.

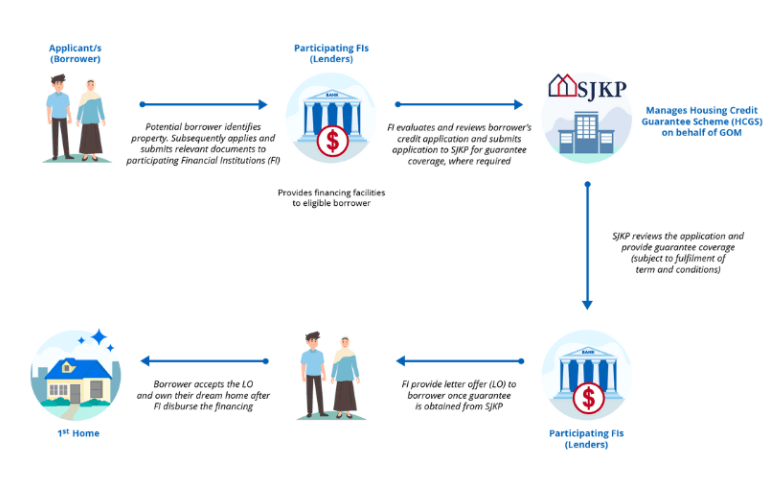

This systemic financial gap frequently leaves vulnerable families trapped in perpetual rental cycles. Without a predictable monthly corporate salary, standard risk assessment models flag these applicants as high-risk, leading to swift rejections. Recognizing this barrier, the Housing Credit Guarantee Scheme—managed through the Sistem Jaminan Kredit Perumahan (SJKP)—has stepped forward to restructure the financing landscape, ensuring that non-traditional earners are not left out of the property market.

Bridging the Risk Gap

The operational brilliance of the scheme lies in how it changes the conversation around financial risk. Rather than forcing applicants to fit into rigid corporate boxes, SJKP essentially acts as an institutional guarantor. If a qualifying first-time homebuyer holds an unconventional income source, the government-backed entity provides a credit guarantee directly to the lending bank.

This state-backed guarantee significantly absorbs the potential default risk for commercial lenders.

With their financial downside fully protected, banks can confidently approve housing applications that would have otherwise been dismissed out of hand. The eligibility framework is deliberately flexible, shifting the focus from corporate documentation to baseline affordability and consistent repayment capacity. With recent federal expansions expanding these guarantees to historic highs, this mechanism has systematically converted banking hesitation into accessible financial pathways for families seeking their very first residential property.

Turning Strategy into Action

However, an ambitious assistance policy is only as effective as its actual grassroots reach. A recurring challenge within many communities is not a lack of eligibility, but a lack of structural awareness. Many eligible gig workers and self-employed individuals simply do not know that these guarantees exist, or they assume that navigating the banking bureaucracy is too complicated to attempt alone.

To dismantle this information gap, community organisations, including the Malaysian Indian Congress (MIC), have initiated targeted outreach campaigns. By mobilising local branch heads and community leaders, the initiative provides direct, localized guidance to walk families through the necessary paperwork. This hands-on strategy ensures that applicants understand how to present alternative proofs of income, such as digital transaction logs or bank statements, effectively removing the intimidation factor from the process.

A Foundation for the Future

Ultimately, accessing a home loan through SJKP is about far more than just securing a set of house keys. Property ownership remains one of the most reliable vehicles for long-term socio-economic mobility. When a family transitions from paying dead-end rent to investing in a permanent asset, their entire financial trajectory changes.

A home offers tangible stability, provides equity that can be leveraged for future generations, and elevates overall living standards. By dismantling the outdated banking barriers that have historically held back non-traditional workers, the scheme ensures that the evolving Malaysian workforce can build a secure, lasting foundation right here at home.